NEWS: 'There Is No Easy Solution'

While the real-estate market is stabilizing, that doesn't mean it's becoming easier for buyers. For those waiting for a return to easy-credit and lots of market churn, it's time to reset expectations.

By Martin Davis

EDITOR-IN-CHIEF

Email Martin

As realtors and real-estate experts gathered in the meeting room on the second floor of the Fredericksburg Area Association of Realtors office Thursday morning, the New York Times issued a breaking news release that should have been music to the ears of those in the room.

“U.S. Mortgage Rates Fall Below 6% for First Time in Years”.

While lower rates are generally welcomed, they are but one marker in a real-estate market that is decidedly different from the one just a decade ago.

That was one of the main point made by the event’s featured speaker, Dr. Jessica Lautz, the deputy chief economist and VP of research at the National Association of Realtors.

“Prior to the pandemic,” she noted, about 5 million housing transactions occurred each year. Now, that number has fallen by 20% to 4 million.

The reasons behind this fall are complex. Contributing factors include:

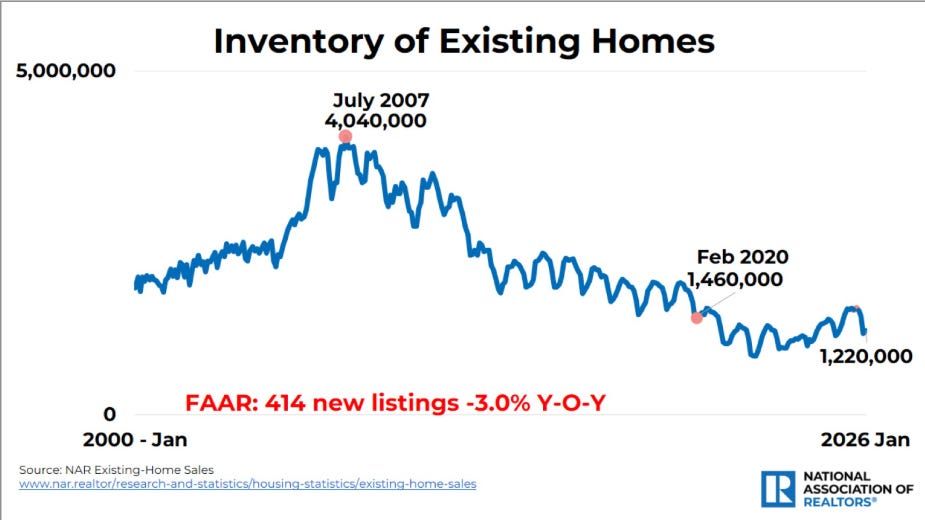

There continues to be a home shortage nationwide of some 4.7 million to 5 million homes

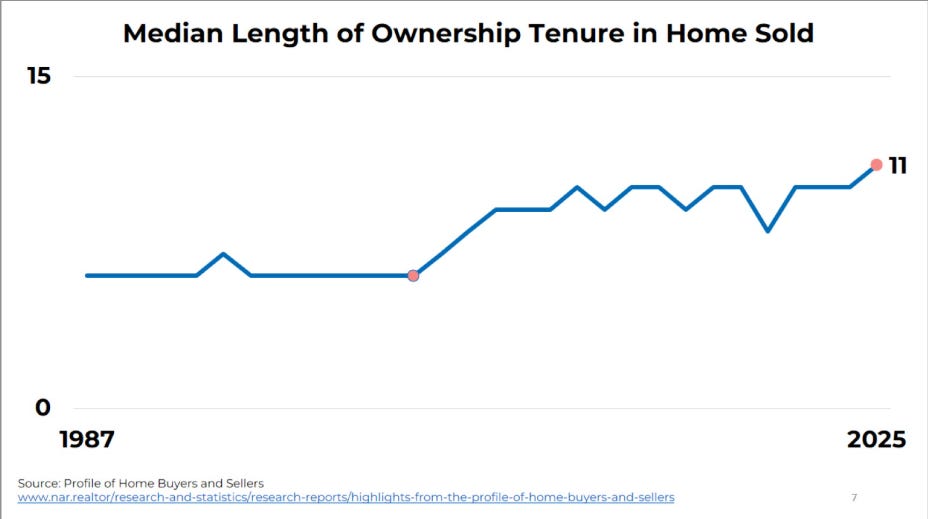

The median length of home ownership is rising, meaning people are staying put

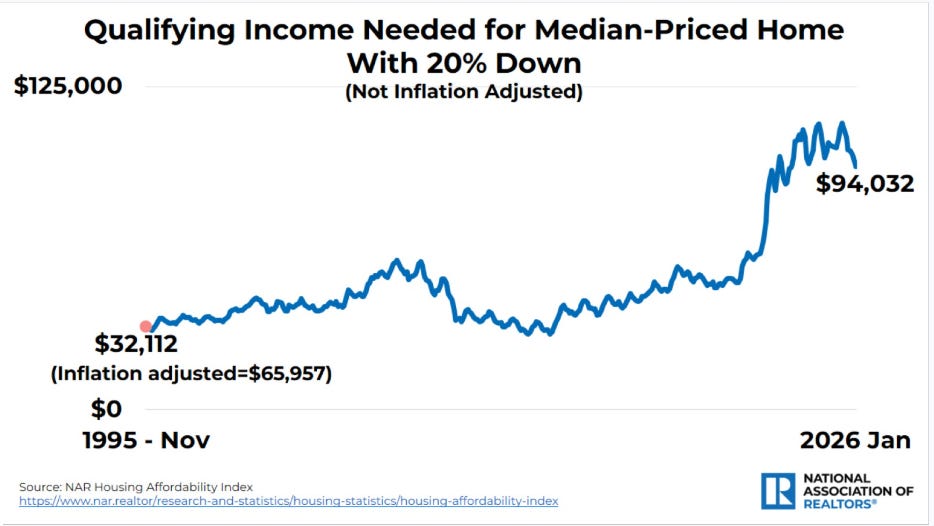

The money required to qualify for a home mortgage is rising

The combination of limited inventory and people staying put longer is putting upward pressure on pricing. That translates to more money required to buy-in to the market.

The consequence is a changing demographic of first-time and repeat homebuyers.

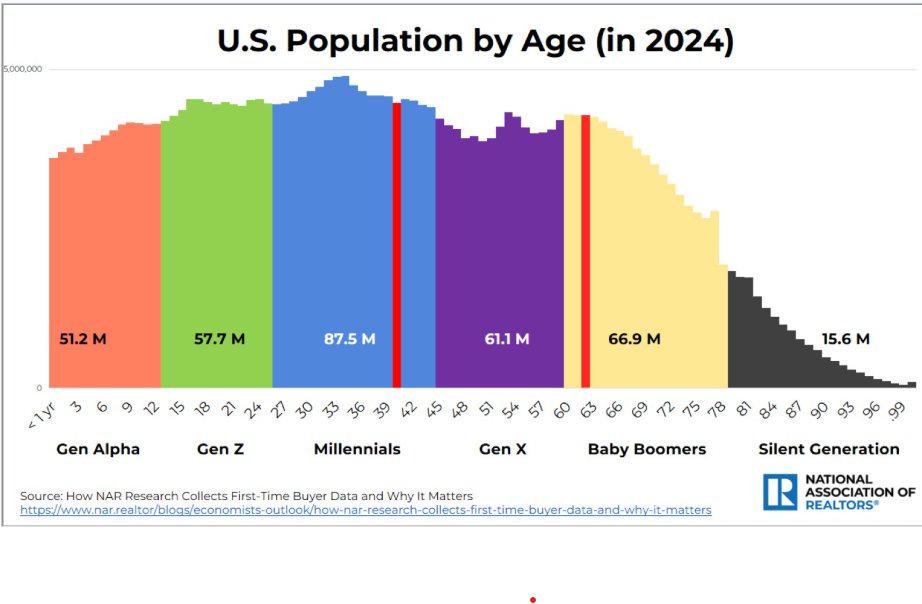

Prior to the Great Recession, the median age of a first-time homebuyer was about 30. Today it’s 40. And the down payment is 10%. Both of these marks are all-time highs.

Repeat buyers are even older — 62, and their downpayments are, on average, 23%. These, too, are all-time highs.

Also noteworthy — just 21% of all homebuyers are first-time homebuyers. That is an all-time low for that statistic.

For homeowners, this all translates to good news. Nationwide, Lautz said, home equity has risen 50% in just over five years.

For those looking to become homeowners, this has proven a trying period.

A ‘Year of Recovery’

The roller coaster ride that the real-estate market has been on in recent years, however, is showing signs of stabilizing some. Lautz said that she expects 2026 to be a “year of recovery.”

A panel discussion led by FAAR President Matthew Rathbun with local Realtors put a human face on what that recovery looks like.

Tamar Myers-Moffatt of Samson Properties described 2025 as a year in two acts. The first half of the year brought first-time buyers who were well-positioned — solid credit scores, cash for down payments — seeking new construction. By the second half of the year, however, she experienced what Lautz’s data highlighted. People leveraging their equity when they felt ready, with first-timers struggling to find a way in. And others choosing to stay put rather than move, which keeps housing stocks tight.

For people with the resources, a tight market isn’t translating into rushed purchases. Yes, supply is down, but so too are the numbers of buyers.

For Denise Smith of Century21 Redwood Realty, this means more time educating both buyers and sellers.

Sellers, she said have to be a bit more patient. Homes are going to sell, she said, but it’s going to take longer. “This gives buyers a bit more control.”

That control gets reflected in adjustments in the seller’s asking price in order to get the buyer to move. Rathbun noted that whereas homes had been selling at 104% of the list price, that number is now closer to 99%.

The seller is still doing well, but they are having to be more responsive to what the buyers are expecting.

Rental Strains

The rental market remains challenging.

Don Pett of Wilkinson Property Management noted that the pool of people applying for leases are facing challenges at a rate higher than in previous periods.

Because Virginia currently allows for higher deposits — up to two months rent — he said, this gives people leasing properties options. If credit is poor but income can be proven and renters can handle the higher deposits, property owners have some latitude to take on a bit more risk in leasing.

That doesn’t help people, however, who will struggle to find those additional deposit funds.

These strains are translating to higher rents and fewer transactions.

In 2019, for example, across all leasing transactions (apartments, single-family homes, etc.) the median rent was about $1,600. That year there were 1,932 rental agreements executed. In 2025, the number of rental agreements was down to 1,645, with the average rent at $2,450.

On the commercial side of the business, Joby Saliceti of BHHS PenFed Realty noted that most commercial transactions are leases.

If leasees aren’t forthcoming, owners, she said, aren’t necessarily motivated to accept less. If they do, it could mean lower profits when the economy starts to turn.

It’s a New Reality

People who first bought when mortgages were freely distributed and sellers could demand what they want, will find a very different reality today.

“There is no easy solution,” Myers-Moffatt said in her comments.

“You can’t walk into WaWa to buy a pack of gum without your wallet. You’re going to have to prepare to buy a house.

That means aggressively working to save or secure money for a down payment, keeping credit scores up, getting that pre-approval letter from the bank, and taking some time to do the work when it comes time to select a house.

For the seller, that means keeping the property in good working order and being open to some negotiation with the buyer.

That tension is actually a healthy one.

So yes, watch those mortgage rates and wait for the right moment. But prepare while waiting, so that when an individual is ready to buy, they can take advantage of the opportunity.

Local Obituaries

To view local obituaries or to send a note to family and loved ones, please visit the link that follows.